Sustainability & Legislation Series - Chapter 6: A Deep Dive into UK Sustainability Standards

By Jesper Risa, Data Analyst, Humans Not Robots.

Sustainability has become a critical factor for organizational success, and having access to clear, practical guidance is more essential than ever. Through our discussions with a range of of organisations, we’ve identified the need to bridge the gap between complex regulations and actionable strategies. This is why we felt there was a need to provide a series of articles to help further understand the intricacies of sustainability legislation and reporting requirements.

Previous series chapters have explored key topics, such as the basics of sustainability and legislation, historical developments, essential terminology, and the emergence of EU sustainability frameworks. Chapter 6 looks at the UK's position.

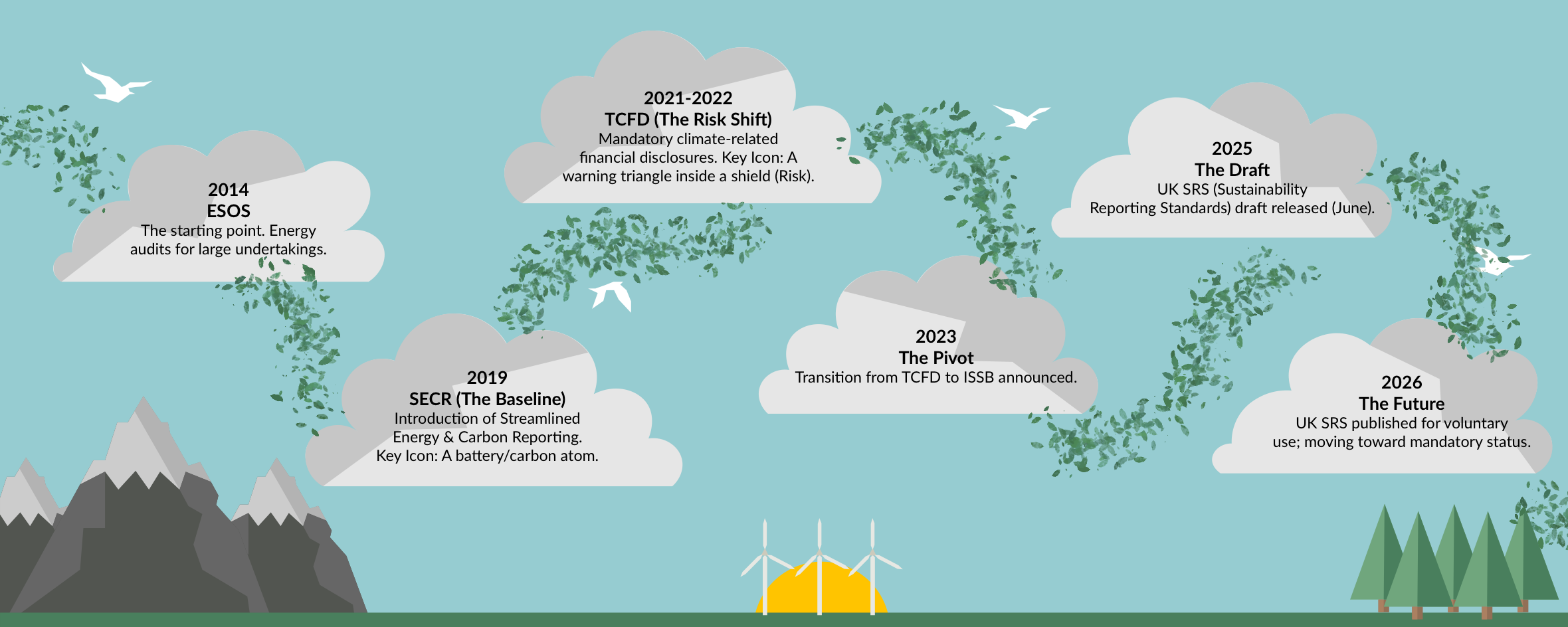

Our home country has a unique history with sustainability reporting legislation, having left the European Union at the end of January 2020. This departure prompted a swift transition from EU reporting rules to the development of new UK-specific legislation.

UK Streamlined Energy and Carbon Reporting (SECR): Requirements, Compliance, and Scope

This transition started in 2019 with the introduction of the ‘Streamlined Energy and Carbon Reporting’ (SECR) rules. These apply to:

- Quoted companies

- Large unquoted companies meeting at least two of the three thresholds: turnover exceeding £36 million, assets over £18 million, and more than 250 employees

- Limited liability partnerships (LLPs)

- Academy trusts

These rules only apply to organisations consuming more than 40,000 kWh of energy in a reporting period.

Organisations covered by SECR must disclose:

- Energy usage

- Carbon footprint

- Greenhouse gas (GHG) emissions

These disclosures must be included in annual financial reports. For quoted companies, the requirements are stricter and include:

- Global scope 1 and 2 GHG emissions (scope 3 is voluntary, but encouraged)

- Global energy usage

- Emissions and energy data from the previous year

- Details of energy efficiency and emissions reduction initiatives

- At least one emissions intensity ratio (e.g., per employee or per £1 million turnover)

- Reporting methodology

Other eligible organisations are only required to report on UK-based energy consumption. If a company cannot report on any required aspect, they must explain why this is the case.

UK TCFD Climate Disclosure Requirements: Mandatory Reporting for British Organisations

The UK introduced the ‘Task Force on Climate-related Financial Disclosures’ (TCFD) reporting requirements in 2021 for premium listed companies, followed by broader implementation in 2022 for:

- The UK’s largest publicly traded companies, banks, insurers, and FCA-regulated pension providers

- Arm’s length bodies (ALBs) with over 500 employees and £500 million turnover, or

- Organisations instructed by their sponsoring department to comply

These organisations must provide an annual risk disclosure covering 11 key areas:

- The board’s oversight of climate-related risks and opportunities

- Management’s role in assessing and managing these risks and opportunities

- Climate-related risks and opportunities identified over the short, medium, and long term

- The impact of these risks and opportunities on the organisation’s business, strategy, and financial planning

- The resilience of the organisation’s strategy under different climate scenarios, including a 2°C or lower scenario

- Processes for identifying and assessing climate-related risks

- Processes for managing these risks

- Integration of climate-related risks into overall risk management

- Metrics used to assess climate-related risks and opportunities

- Scope 1, 2, and, where relevant, scope 3 GHG emissions and related risks

- Targets for managing climate-related risks and opportunities, and progress against these targets

UK Sustainability Reporting Standards (SRS): ISSB Alignment and Future Compliance Requirements

In July 2023, it was announced that the TCFD framework had been completed, and the UK would transition fully to the ‘International Sustainability Standards Board’ (ISSB) standards. These standards, referred to as ‘UK Sustainability Reporting Standards’ (UK SRS), are set to be published for voluntary use in early 2026, following a draft release in June 2025. The UK SRS is expected to eventually become mandatory for large private companies, LLPs, quoted companies, and public interest entities (PIEs).

The standards are divided into two main areas:

- S1 – General sustainability disclosures

- S2 – Climate-related disclosures

S1 focuses on disclosing information about how sustainability-related risks and opportunities impact enterprise value. It requires organisations to detail governance, strategy, and risk management processes related to sustainability, as well as metrics and targets for monitoring and managing risks. These disclosures must encompass the entire value chain and ensure alignment with financial reporting.

S2 addresses climate-specific risks and opportunities, requiring organisations to identify and disclose physical and transition risks. It includes details of how these risks affect financial performance, transition planning, climate resilience, and scope 1, 2, and 3 emissions.

Additional UK Sustainability Legislation and Regulatory Frameworks

Beyond the legislation already discussed, the UK has implemented several other important regulations in recent years.

Following its exit from the EU, the UK replaced EU sustainability laws with its own ‘Environmental Act’. This legislation covers a wide range of areas, including:

- Long-term environmental improvement targets

- Waste and resource efficiency (e.g., recycling and litter enforcement)

- Air quality measures

- Strengthened duties for public bodies to conserve and enhance biodiversity, including mandating a ‘net gain’ for biodiversity

The ‘Energy Savings Opportunity Scheme’ (ESOS) requires qualifying organisations to conduct energy audits every four years to identify opportunities for energy savings. Introduced in 2014, ESOS applies to large undertakings.

Additionally, the UK government mandates compliance with the ‘Sustainability Reporting Guidance 2025-26’. This document outlines the minimum requirements and guidelines for sustainability reporting across government bodies, reflecting the government’s commitment to sustainable practices within its own operations.

Sustainability reporting is rapidly gaining prominence and scope in the UK. This shift creates an opportunity for British organisations to move away from inefficient practices, reducing wasted time and resources. However, it also means that accurately measuring and analysing business-related sustainability metrics is more critical than ever. At Humans Not Robots, we simplify this process, using AI-powered analytics to model, understand, and optimise carbon emissions and costs across your organisation’s technology footprint.

Get in touch with us today to explore how we can help you understand and leverage your sustainability data and improve your business performance.

Related News

We measured our own carbon footprint. Here is what we found

The Future of Media is Hybrid: Inside the 5G-EMERGE Service Platform

Sustainability & Legislation Series - Chapter 8: US Sustainability Reporting in 2026: Fragmented Rules, Rising Stakes

Ready To Start Saving?

Talk to HNR to reduce carbon emissions and costs from your digital infrastructure.

Book Demo